Hospital-Based Services Arrangements: Trends and Strategic Implications for Healthcare Systems

Explore key trends, operational challenges, and data-driven strategies for sustainable support.

Hospitals and healthcare systems are increasingly challenged by rising costs to support hospital-based specialties, including emergency medicine, hospital medicine, anesthesiology, and radiology. Traditionally, these specialties generated sufficient revenue to cover operational costs. However, over the last four years, primarily since 2020, hospital-based practices have faced declining revenue streams, rising operating expenses, and increasing provider compensation. This article examines the underlying economic forces driving these changes and presents strategic insights for hospital executives and legal counsel.

Compensation Trends and Productivity

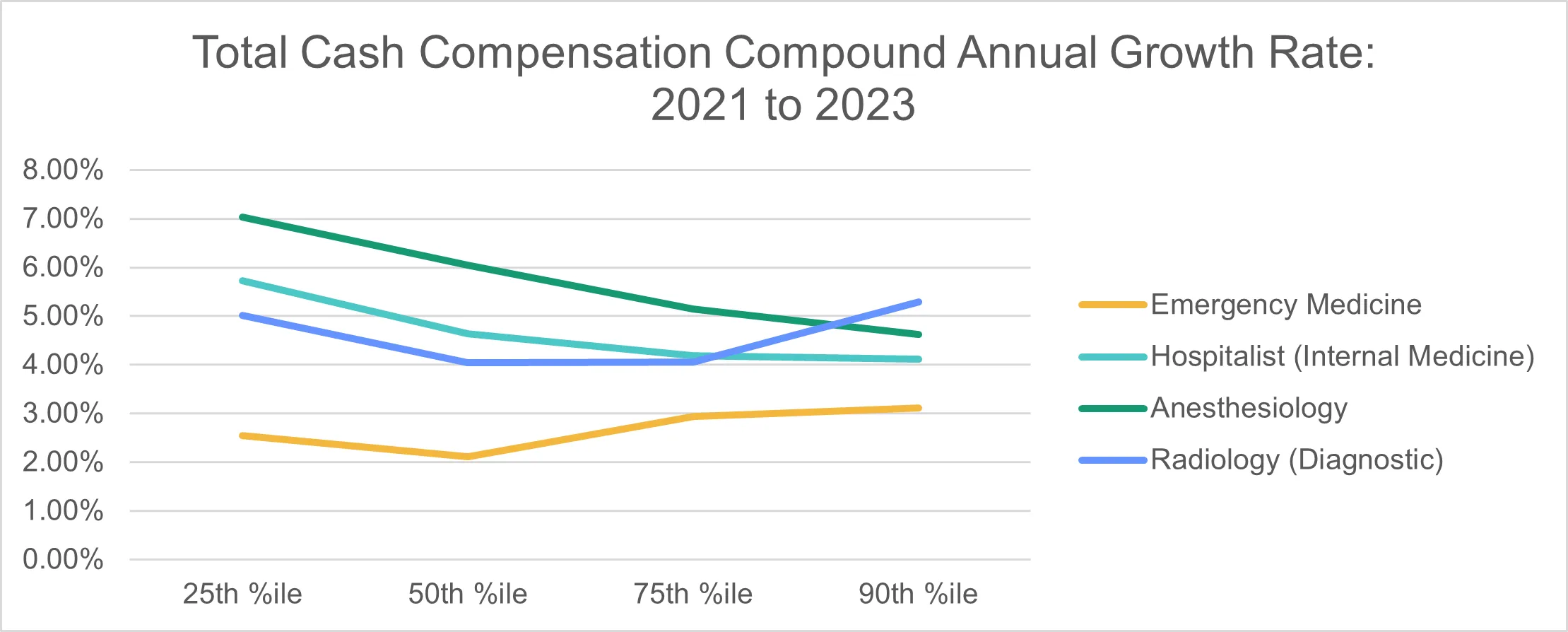

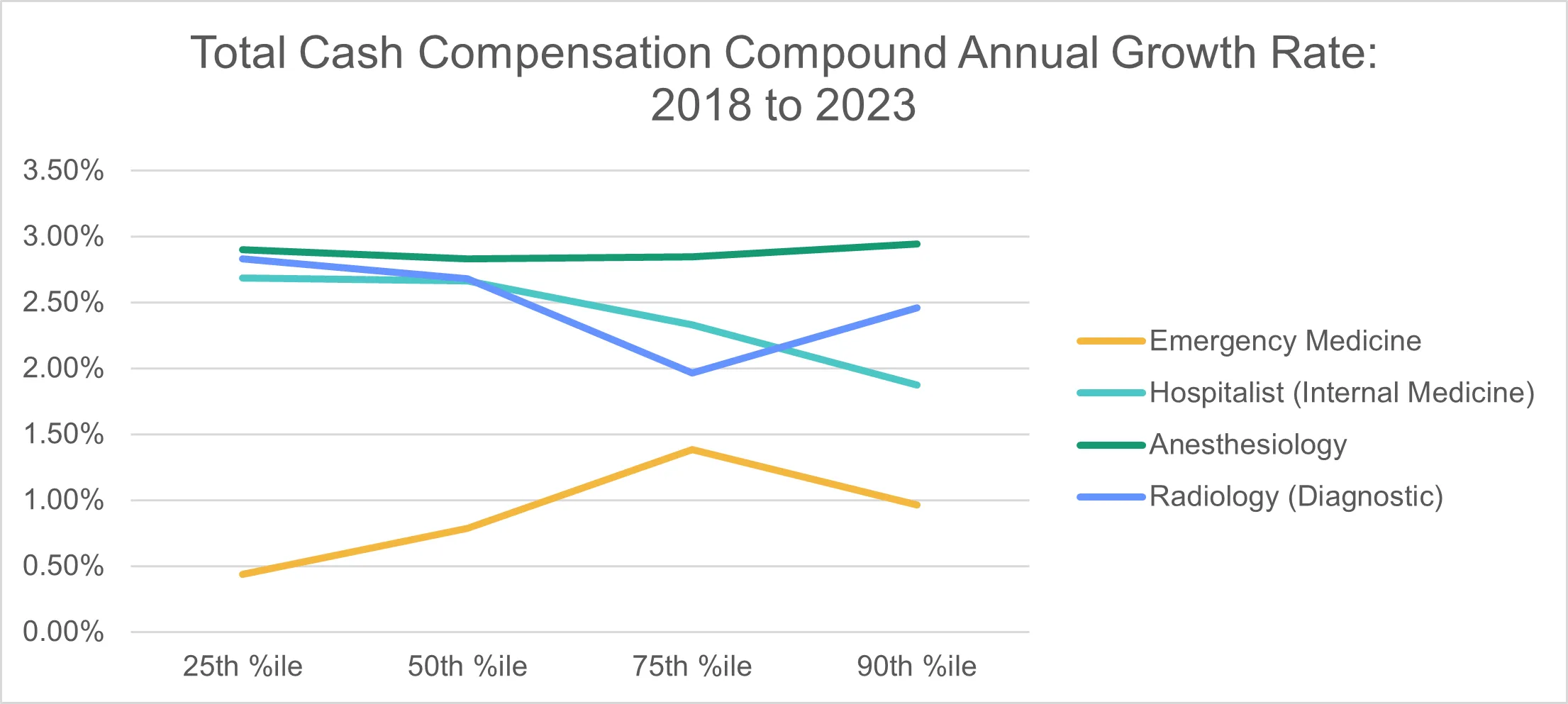

Physician cash compensation has steadily increased across hospital-based specialties. Analysis over the recent two- and five-year periods shows a consistent growth trajectory, with cash compensation likely to continue rising by at least 3% annually despite variations across specific percentiles (Figures 1 and 2). [1]

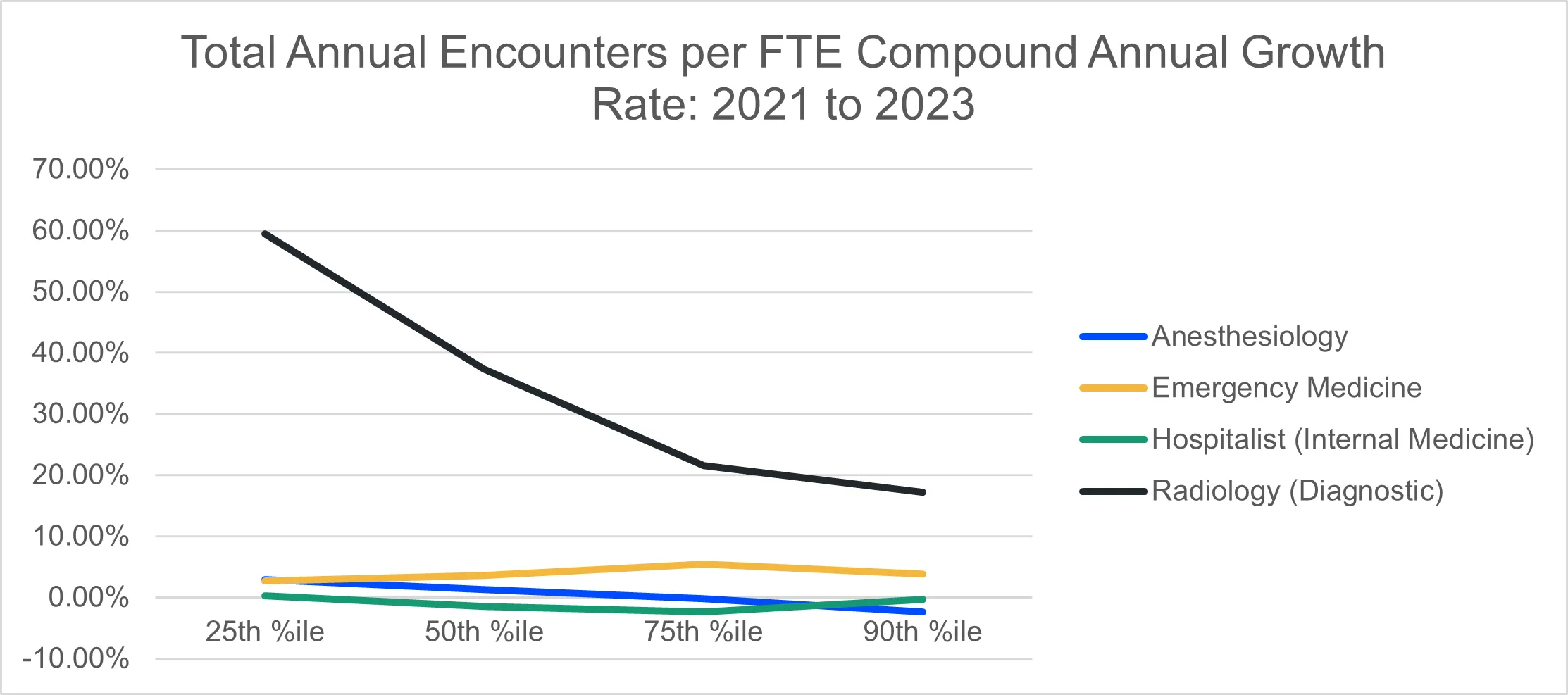

Productivity metrics further illustrate these changes. While telemedicine has notably increased total encounters per FTE physician in radiology, encounter growth in emergency medicine, hospital medicine, and anesthesiology remains moderate at around 5% per year. A return to pre-pandemic service levels and demographic factors, such as population growth and aging, may influence this upward trend. (Figure 3) However, these increases in patient volume may ultimately be offset by reimbursement reductions in the coming years. [2]

Reimbursement Reductions Across Hospital-Based Specialties

A 2024 review of national reimbursement rates reveals significant decreases in Medicare reimbursement for frequently billed CPT codes across all major hospital-based specialties. [3] When comparing 2024 rates with those from 2020, we observe the following reductions:

- Radiology: -8.63%

- Emergency Medicine: -4.62%

- Hospital Medicine: -6.18%

- Anesthesiology: -9.52% [5]

The Centers for Medicare & Medicaid Services (CMS) has recently implemented rules that may reduce reimbursement by 2.93% for certain services. [4] Given these downward adjustments, hospitals must carefully assess their compensation and support models for these specialties to mitigate revenue losses.

Inflation and Cost Increases in Practice Operations

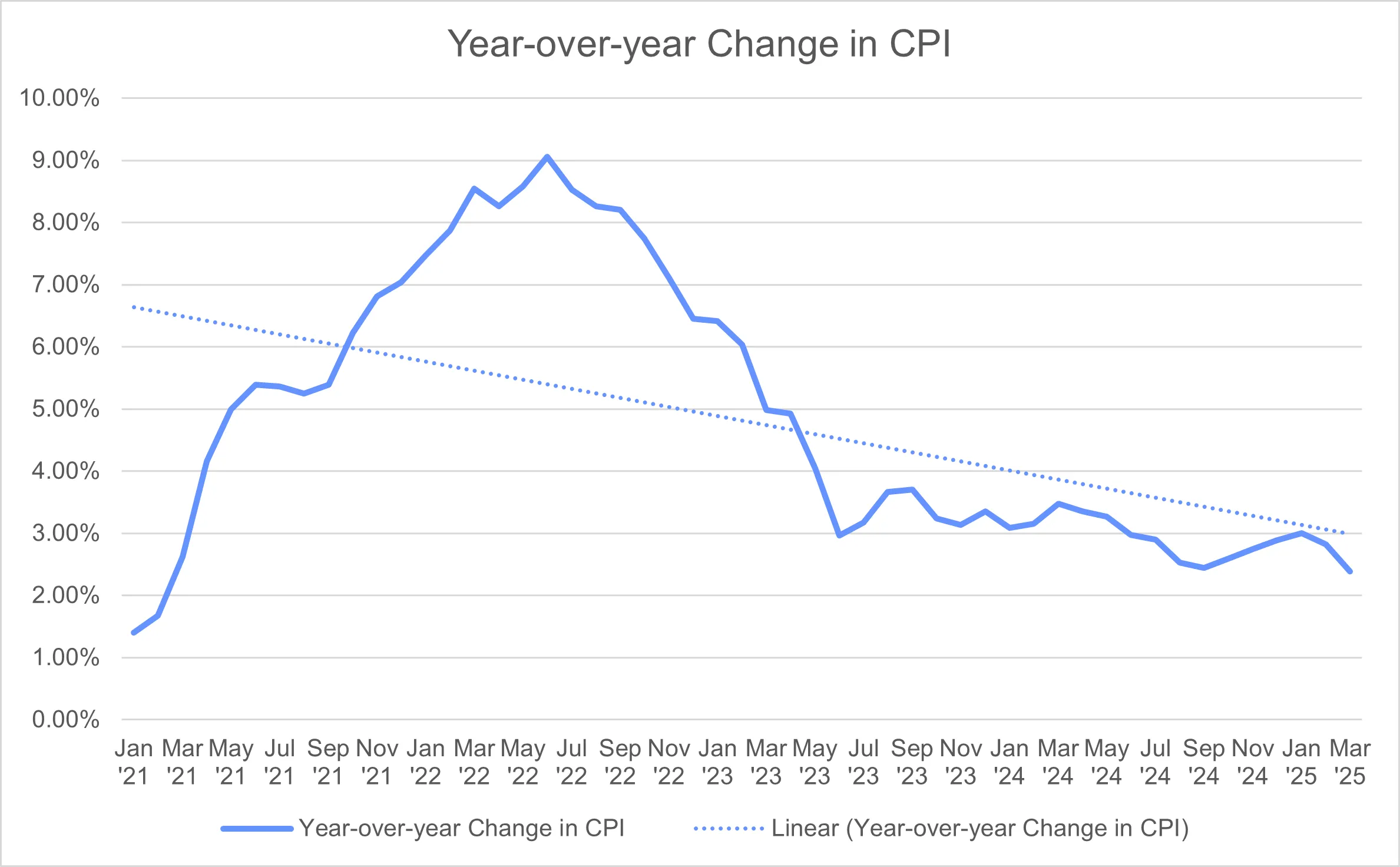

Contracts for hospital-based specialties have evolved to reflect the impacts of inflation. Historically, most service agreements did not include automatic price adjustments, but this trend has shifted since 2020. Contracts now often feature provisions for annual increases tied to the lesser of a fixed percentage (typically 2%-3%) or the Consumer Price Index (CPI). Although CPI and Producer Price Index (PPI) inflation rates have shown signs of deceleration, the overall impact on operating costs remains significant. (Figure 4) [6]

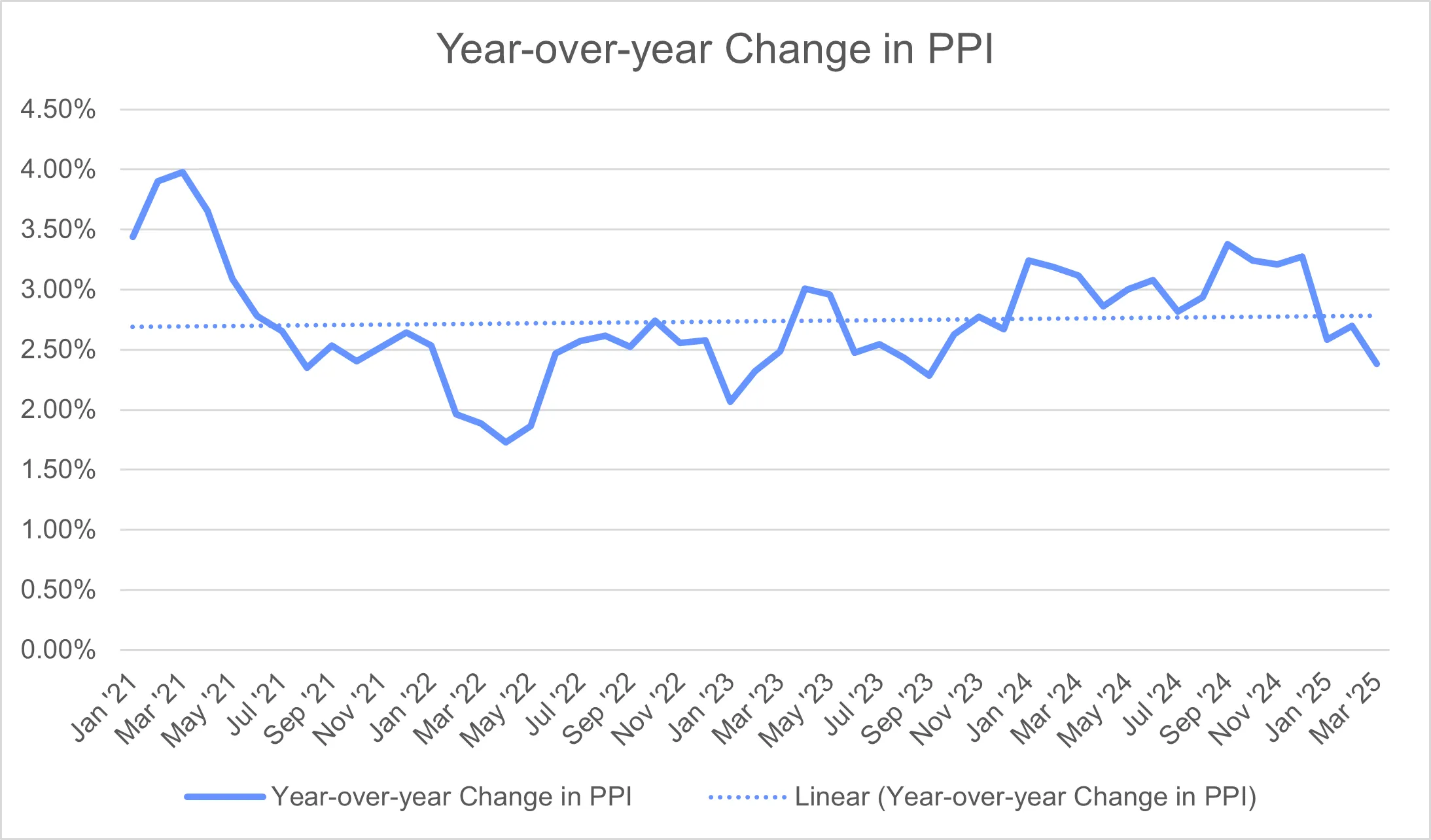

The CPI for urban consumers has increased at an annual rate of 4.98% from January 2021 to January 2025, while the PPI for selected healthcare industries has risen by 2.61% over the same period. (Figure 5) [6,7] This inflationary pressure has driven up practice operating costs, particularly in hospital medicine, which saw a 28.7% compound annual growth rate at the median, according to MGMA Cost and Revenue Reports. [8]

Workforce Dynamics and Provider Burnout

Changes in workforce dynamics, including focusing on provider well-being, have reduced the hours FTE physicians and advanced practice providers (APPs) worked. To maintain service levels, hospitals and practices increasingly rely on additional staffing, which further contributes to rising provider costs. Addressing provider burnout through scheduling adjustments and support initiatives has become a priority. Yet, it also imposes financial challenges, as additional FTEs may be necessary to compensate for reduced individual productivity. [9]

Strategic Recommendations for Hospital Executives

Given the increasing cost burdens and revenue constraints associated with hospital-based specialties, healthcare executives should consider the following strategic measures to manage financial impact:

- Optimize Reimbursement Negotiations: Monitor upcoming CMS changes closely and prepare to negotiate with private payers to offset potential losses in Medicare revenue.

- Implement Sustainable Staffing Models: Proactively address provider burnout by developing flexible staffing arrangements, including cross-coverage and shift optimization, while evaluating cost-effective ways to maintain care quality.

- Adopt Contractual Inflation Adjustments: Ensure future contracts include inflation-adjusted clauses for both CPI and PPI, with maximum thresholds to control costs.

- Leverage Data to Monitor Financial Metrics: Regularly track metrics, such as CPT code volume changes, productivity rates, and overall operating costs, using MGMA and CMS data to stay informed of trends and adjust financial planning accordingly.

Conclusion

The financial support required for hospital-based specialties is projected to grow through 2025, fueled by rising compensation and operating costs as well as reimbursement cuts. Hospitals must adapt by adopting efficient staffing models, monitoring financial indicators, and building flexible contractual agreements. By doing so, healthcare systems can better navigate the economic challenges in supporting essential hospital-based specialties.

References

- Medical Group Management Association (“MGMA”): Provider Compensation Survey, 2019 through 2024, based on 2018 through 2023 data for Total Cash Compensation: Anesthesiology, Emergency Medicine, Hospitalist: Internal Medicine, and Radiology: Diagnostic; American Medical Group Association (“AMGA”): Medical Group Compensation and Productivity Survey, 2019 through 2024 Total Cash Compensation for Anesthesiology, Emergency Medicine, Hospitalist – Internal Medicine, and Radiology – MD Non-Interventional; SullivanCotter (“SC”) Physician Compensation and Productivity Survey, 2019 through 2024 Total Cash Compensation for Anesthesiology, Emergency Medicine, Hospitalist – Internal Medicine, and Radiology – Diagnostic.

- MGMA: Provider Compensation Survey, 2019 through 2024, based on 2018 through 2023 data for Total Encounters per FTE Physician: Anesthesiology, Emergency Medicine, Hospitalist: Internal Medicine, and Radiology: Diagnostic.

- Centers for Medicare & Medicaid Services (“CMS”), Physician Fee Schedule for Calendar Years 2024 and 2020.

- CMS, Calendar Year (CY) 2025 Medicare Physician Fee Schedule Proposed Rule, July 8, 2024, available at: https://www.cms.gov/newsroom/fact-sheets/calendar-year-cy-2025-medicare-physician-fee-schedule-proposed-rule.

- Based on national anesthesiology conversion factors by location.

- Bureau of Labor Statistics (“BLS”), Consumer Price Index, last accessed May 5, 2025, https://www.bls.gov/cpi/.

- BLS, Producer Price Indexes, last accessed May 5, 2025, https://www.bls.gov/ppi/. PPI for December 2024 through March 2025 based upon preliminary data.

- Per BLS, August 2024 PPI figures are preliminary and subject to revision up to four (4) months after original publication.

- MGMA Cost and Revenue Report, 2022-2024 Surveys based on 2021-2023 data.